Blog

This question was asked recently:

“Where do I find resources that explain the A, B, C of personal finance in the U.S., where to start, what’s a good plan, what are crucial elements you need to consider, and what do you absolutely need to start doing now (the right way)?

It’s an honest question, and a necessary one.

If you have ever felt overwhelmed by terms like credit scores, emergency funds, savings plans, or investing, you’re not alone. Personal finance in the U.S. isn’t always intuitive, and people learn by making costly mistakes. For many people, especially immigrants and first-generation earners, personal finance in the U.S. feels like being dropped into the middle of a game with no instructions. Everyone else seems to know the rules. You’re working hard, earning income, paying bills, but you are unsure whether you are actually building anything.

Let’s slow this down and walk through it clearly.

First, a Truth You Need to Hear

Personal finance in the U.S. is not hard because you are incapable.

Most people learn:

- About credit after damaging it

- About taxes after penalties

- About investing after years of delay

The goal is not to know everything.

The goal is to understand the right sequence, and early at that.

This exact question, where to start and what order to follow, is why we created The Money Start. It’s designed for people who don’t need advanced strategies yet, but clarity. Instead of scattered advice, it walks through the foundations of personal finance in the U.S. step by step, helping you build awareness, structure, and confidence before moving on to anything complex.

The A, B, C of Personal Finance (U.S. Edition)

Think of personal finance like building a house. You don’t start with furniture. You start with the foundation.

A — Awareness: Know Your Starting Point

Before you can create a plan, you have to understand where you are.

Most people think if they earn money, they are on the right path. The truth is more nuanced. Almost half of U.S. adults would not be able to pay a $1,000 emergency expense without borrowing or using credit, which tells us something important about financial preparedness.

A good place to begin is by answering a few key questions:

- How much do I currently earn and spend each month?

- What debts do I have, and at what interest rates?

- Do I have any savings, and if so, for what purpose?

- What’s my credit history and credit score?

This kind of awareness brings clarity — and clarity is the foundation of financial progress.

Helpful resources:

- AnnualCreditReport.com (free, official credit reports)

- Your bank’s spending insights or simple tracking apps

- IRS website (basic understanding of taxes and withholdings)

If you don’t know your numbers, your money will always feel stressful.

B — Build the Basics: Emergency Funds & Budgeting

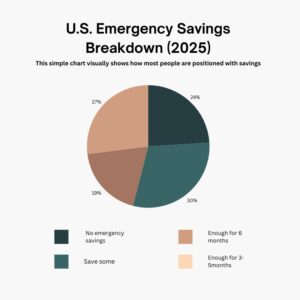

Once you know where you stand, the first system you should build is a basic financial structure, starting with savings and budgeting. Emergency funds are one of the most practical financial habits you can develop. While the ideal recommendation is to save three to six months of living expenses, data shows that many Americans haven’t reached that mark yet. Only about 46% have enough savings to cover three months of expenses, and nearly a quarter have no emergency savings at all.

That’s not just a statistic, it’s a prompt to build your financial buffer.

When you have an emergency fund:

- You avoid relying on credit cards with high interest.

- You reduce stress when unexpected costs arise.

- You protect your long-term plans from short-term shocks.

In many surveys, more than half of respondents say they rely on credit cards to pay for urgent expenses, even for amounts as small as $500. This highlights how essential a savings plan is early on.

Budgeting goes hand in hand with savings. While traditional rules like 50/30/20 used to guide many people, newer approaches like the 60/30/10 method reflect today’s reality, especially in high-cost areas, where necessities take a larger share of income.

The key isn’t perfect budgeting, but consistent budgeting, having a system you revisit regularly.

C — Credit: Understand It Before You Use It.

In the U.S., credit isn’t just a number, it’s a tool that determines access to housing, loans, jobs, and more. But many people jump into credit without understanding the rules, costs, or consequences. This often leads to expensive debt cycles.

U.S. household debt amounts to trillions of dollars, and credit card balances alone surpass $1 trillion. Meanwhile, many households don’t have enough savings to cover emergencies, creating a cycle where credit becomes the fallback.

Understanding credit means knowing:

- What affects your score (payment history, utilization, length of credit)

- How interest rates work

- How to build credit responsibly

Credit isn’t inherently bad, but misunderstanding it can cost you dearly.

Practical Steps to Take Now (The Right Way)

Here’s what you can begin doing today:

- Track your finances weekly.

You don’t need perfect budgets, just clarity on where money is coming from and where it’s going. - Open a separate savings account.

Even if you start with $25 a week, consistency builds over time. - Review your credit report.

One free report per year is available at AnnualCreditReport.com, know what’s on yours. - Protect against emergencies.

Aim first for a small emergency buffer, then build toward that 3–6 month goal. - Learn before you invest.

Investing without fundamentals is like building a house without a foundation.

Consistency & Long-Term Thinking

Once you have established awareness, basic savings, and responsible credit habits, the next step is consistency.

Personal finance isn’t about one good decision, it’s about good decisions repeated over time. A plan focused on survival only gets you so far. A plan focused on structure, with clear savings, debt repayment, and investing goals, becomes sustainable wealth-building.

Even as the U.S. economy grows and household wealth reaches record levels, individual financial health varies dramatically. The difference often comes down to systems, not just income. Systems make actions repeatable, ensuring they reduce confusion. They make your money work for you instead of you working for money.

Source: Bankrate Emergency Savings Survey, 2025