Blog

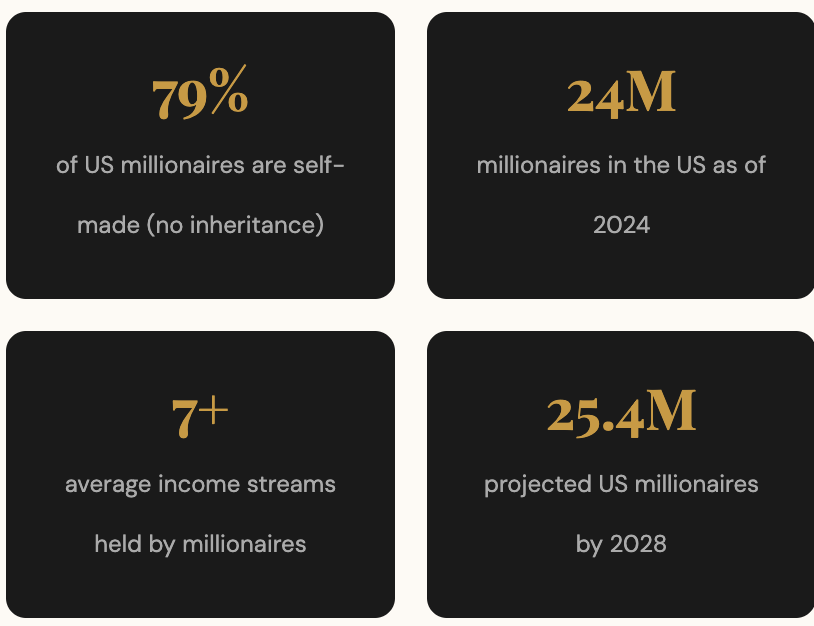

The number of millionaires in America grew from 7.64 million in 2020 to nearly 24 million in 2024 — and you don’t need to have been born rich to be counted among them.

Statistics tell a powerful story: 79% of American millionaires are self-made. They started from zero. No trust funds. No generational wealth. Just knowledge, systems, and consistency. As an immigrant, you already have the work ethic. What most of us lack is the financial roadmap that Americans often absorb from childhood.

1. Believe It Is Possible — The Mindset Foundation

Before strategy, there must be belief. The single biggest barrier for most immigrants isn’t lack of opportunity — it’s a mental ceiling. When your first salary in America feels like riches compared to back home, it’s easy to stop dreaming bigger.2. Understand That Wealth Is Built Over Time

One of the most dangerous beliefs circulating in immigrant communities is the idea of “getting rich quick.” Urgency leads to vulnerability. Scammers specifically target immigrants who are behind financially and are looking for shortcuts. The truth is wealth is slow, gradual, and extremely intentional. There are no shortcuts — only systems that compound over time. Starting early makes an enormous difference. An immigrant who arrives at age 30 and begins investing $200/month immediately will still accumulate over $450,000 by age 60 — but only if they start now.3. Track Every Dollar — Budget Like a Millionaire

Most people know what they earn. Very few know what they spend. This gap is where wealth goes to die. Spontaneous spending — clicking “buy” on a 50%-off Amazon deal without planning — erodes savings invisibly. Millionaires don’t budget because they’re rich. They’re rich partly because they budget. The practice of tracking income and expenditure is not about deprivation — it’s about intentionality.- Write down every source of income and every category of spending: rent, food, subscriptions, entertainment.

- Save 5–10% of every paycheck automatically before you spend anything else.

- Move savings to a high-yield savings account (HYSAs typically offer 4–5% APY vs. near-zero in regular banks).

- Use free apps like YNAB, Mint, or a simple Google Sheet to track spending weekly.

4. Build Your Credit History

In America, credit is currency. Your credit score determines whether you can rent an apartment, get a car loan, buy a house, or even qualify for certain insurance plans. Many immigrants arrive without any US credit history, which means starting from scratch. A common story: arriving, getting a first credit card, maxing it out without understanding the consequences, then discovering a damaged score only when trying to rent a first apartment. Avoid this by following these steps:- Get a secured credit card immediately: deposit $200–$500, use it for small purchases like gas or groceries.

- Never exceed 10–30% of your credit limit: this is called credit utilization and heavily impacts your score.

- Pay on time, every time: payment history accounts for 35% of your FICO score.

- Keep old accounts open: the length of credit history matters. Don’t close your first card.

5. Intentionally Increase Your Skills

You don’t need to know everything to start. You just need to be willing to learn. In the digital economy, skills translate directly into income streams. Some of the highest-demand, self-learnable skills in 2026 include:- Content creation: YouTube, TikTok, Instagram — build an audience around your expertise.

- Stock trading / investing: Learn technical analysis, ETFs, and index fund investing.

- Amazon FBA / KDP / Print-on-Demand: Sell physical or digital products using Amazon’s distribution network.

- Freelancing: Offer services on Fiverr or Upwork using skills from your day job (writing, design, accounting, coding).

- Affiliate marketing: Earn commissions promoting products you already use and believe in.

6. Start Investing Early — Let Time Do the Heavy Lifting

You don’t need to be wealthy to start investing. You need to start investing to become wealthy. The S&P 500, which tracks the 500 largest US companies, has historically returned an average of 10% per year. Index funds like SPY or VOO let you buy a slice of all 500 companies with a single purchase. The gap between starting 10 years earlier is over $800,000 — not from putting in more money, but from giving compound interest more time to work. Automate your investments so consistency is built into your system, not your willpower.7. Supplement Income & Protect What You Build

The average millionaire has 7 streams of income. Most start with one — their day job — and intentionally build others. In 2026’s distribution economy, you don’t need permission to start a business. Amazon, Shopify, YouTube, and Fiverr are all free to join. Once you begin building, protect what you’ve created:- Health insurance: one medical emergency without coverage can wipe years of savings.

- Life insurance: term life is affordable and protects your family’s financial future.

- Car insurance: legally required and financially essential.

- Emergency fund: keep 3–6 months of expenses in a liquid, accessible account.

Finally: build generational wealth. Teach your children what you are learning. The knowledge you gain today can change your family’s financial trajectory for generations.